sankai

Investment Thesis

ON Semiconductor (NASDAQ:ON) got hit with a downgrade recently and the analyst pointed out some valid concerns. That being said, ON Semiconductor has been executing well on their strategic plans and are positioned to capitalize on growth in SiC demand. We believe the current weakness is a good opportunity for long-term investors to buy shares.

Analyst Downgrade

William Blair recently downgraded ON Semiconductor to market perform from outperform. The analyst responsible for the call had some valid concerns but the bull case for ON Semi is about long-term SiC demand trends and the analyst’s downgrade mostly focused on short-term concerns. Seeking Alpha published a great summary about this piece of news and we are going to go through the points the analyst made and why the long-term bull case around ON’s strategic positioning and SiC demand growth prevails. (Points paraphrased for brevity)

1. “The recent increase in cost of capital globally undermines William Blair’s confidence in the auto and industrial markets that are served by ON’s traditional silicon business.”

The economy goes through cycles and the semiconductor industry is cyclical in nature. It is to be expected that there are peaks and troughs in demand. The relevant factor is whether or not demand is creating higher highs and higher lows over the course of many cycles. As long as the current trough is higher than the trough of the last cycle, overall demand for semiconductors is increasing. EVs share of the auto market will increase over the next decade so it is difficult to see this downturn being more than just a blip. It’s also unlikely to see any sustained weakness in the industrial market as many manufacturing processes rely on semiconductors and the companies will purchase them regardless of the cost of capital because they are economically necessary. There is valid reason for a loss of confidence in the short term but owners of the stock should understand the tailwinds in play and that the bull case is a long-term one. Investors shouldn’t be deterred by temporary weakness in some of ON’s end markets.

ON Semi Q3 Earnings Presentation

{kind=link}

2. “With the combination of a weakening traditional business and lower silicon carbide yields, ON Semiconductor’s gross margins could fall to 45% or below.”

Gross margin compression could definitely be on the horizon, but this goes back to the cyclical nature of the industry and the economy. Any compression in gross margins would likely reverse itself in a year or less.

3. “Silicon carbide yields at GT Advanced Technologies could be as low as 15% to 20%, half of the 30% that was initially estimated. That could be an issue for ON Semiconductor and its supply agreements with other companies, including Tesla (TSLA). And given that much of its wafer supply for automotive is already spoken for, the company is stuck between a “rock, hard place, and another harder place,” Dorsheimer suggested.”

ON Semi acquired GT Advanced Technologies for $415 million in cash back in 2021. This acquisition was done with the intention of strengthening ON Semi’s SiC portfolio and is a good move from a strategic point of view. If it is indeed true that their yields are coming in below expectations it would be a significant impediment to ON Semi’s plans in the short term. They will need to improve their yields going forward or else large customers that buy in advance may be concerned a future order might not get filled and will opt to sign supply agreements with competitors. This is a black eye to the bull case if true and the company will need to improve their manufacturing efficiency in the future.

4. “The way he sees it, ON Semiconductor has three options: they can make up for low yields with higher internal volume, shorten cycle times and put more cash into furnaces; they can extend their existing long-term supply agreements with Wolfspeed (WOLF) or Rohm; or they can miss production targets and jeopardize their agreements, viewed as the most unlikely.”

It seems likely ON Semi will invest into more capacity while also working to improve their efficiency. While this could lead to having too much supply it is the best long-term solution to ensure that all orders will be able to be filled. I prefer this approach to extending their supply agreements with Wolfspeed or Rohm which is a band aid solution. Doing the hard work to get manufacturing right is one step that ON needs to take to become a long-term winner in SiC. There will be short-term pain but ideally the gain will be worth it, as long as they can execute.

Strategic Vision and Execution

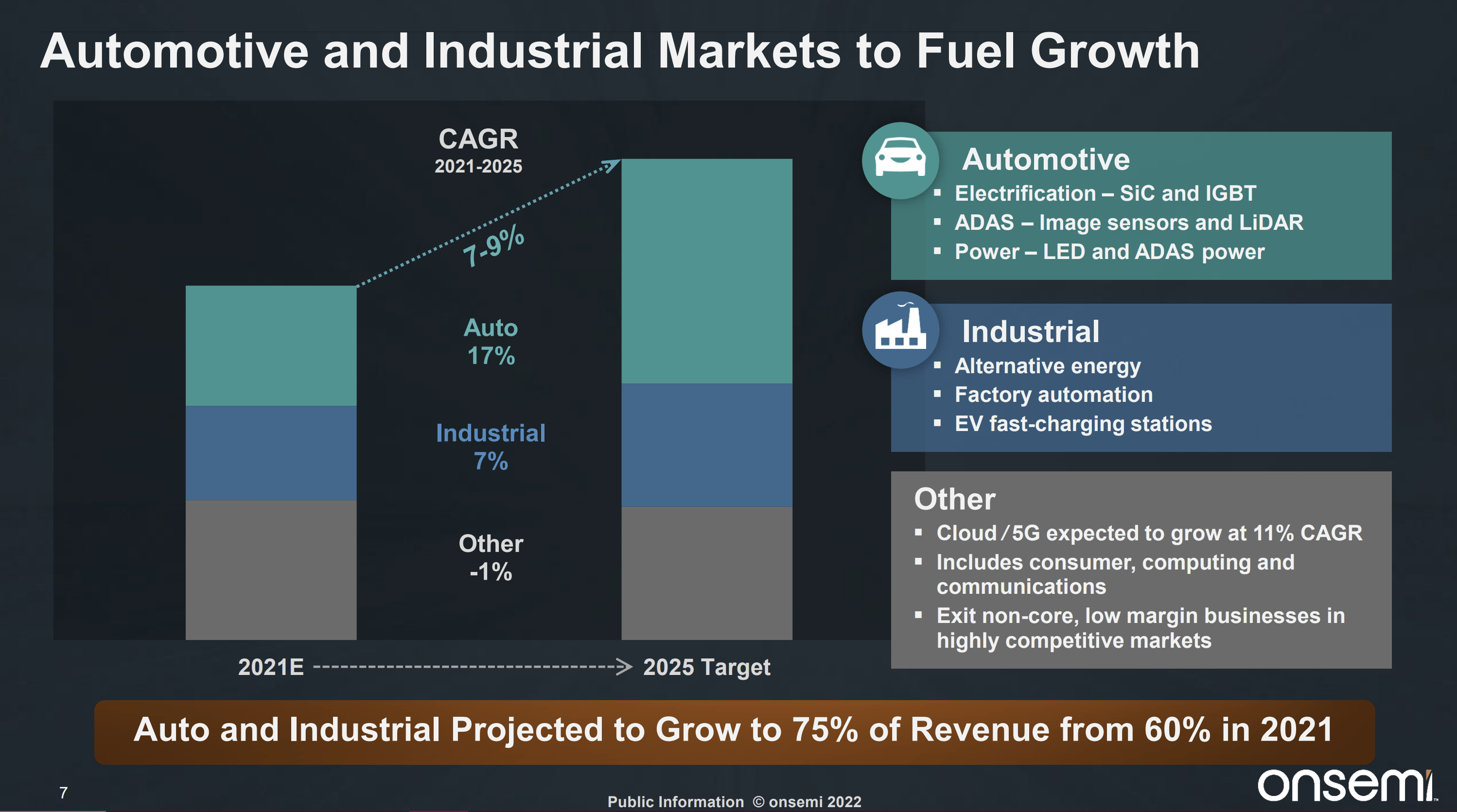

The below slide is a great insight into what the management of ON Semi is focused on. The automotive and industrial segments of their business are the fastest growing parts and they are working to give more operational focus to those segments. They have experienced a large amount of gross margin expansion in the past but have plateaued on that front over the past few quarters. Their gross margins are expected to decrease going forward.

ON Semi Q3 Earnings Presentation

{kind=link}

The goal of ON Semi is to be the strongest player in the SiC space and they have chosen to focus their resources on the automotive and industrial end markets.

ON Semi Q3 Earnings Presentation

{kind=link}

These graphics are taken from ON Semi’s website. I encourage all investors doing their due diligence to go check it out. Their website is full of informative material to help you better understand the business and to decide for yourself what you think of the company.

ON Semi Website ON Semi Website ON Semi Website

{kind=link}

{kind=link}

{kind=link}

Financial Results

The financial results were negatively impacted by goodwill and intangible asset impairment of $271.8 million.

From ON Semi’s Q3 earnings report:

On September 16, 2022, the Company’s Board of Directors approved an exit plan to wind down the QCS division as part of its ongoing efforts to focus on growth drivers and key markets, and to streamline its operations.

This wind down is in line with their strategic vision and will likely benefit the company over the long term.

Quarterly operating income would have been $696.3 million if this impairment did not take place. That’s compared to $399.2 million of operating income in the year ago period. So while on the surface it looked like there was not much operating profit growth, a closer inspection shows that ON Semi is taking some short term pain to prepare their organization for the fight ahead.

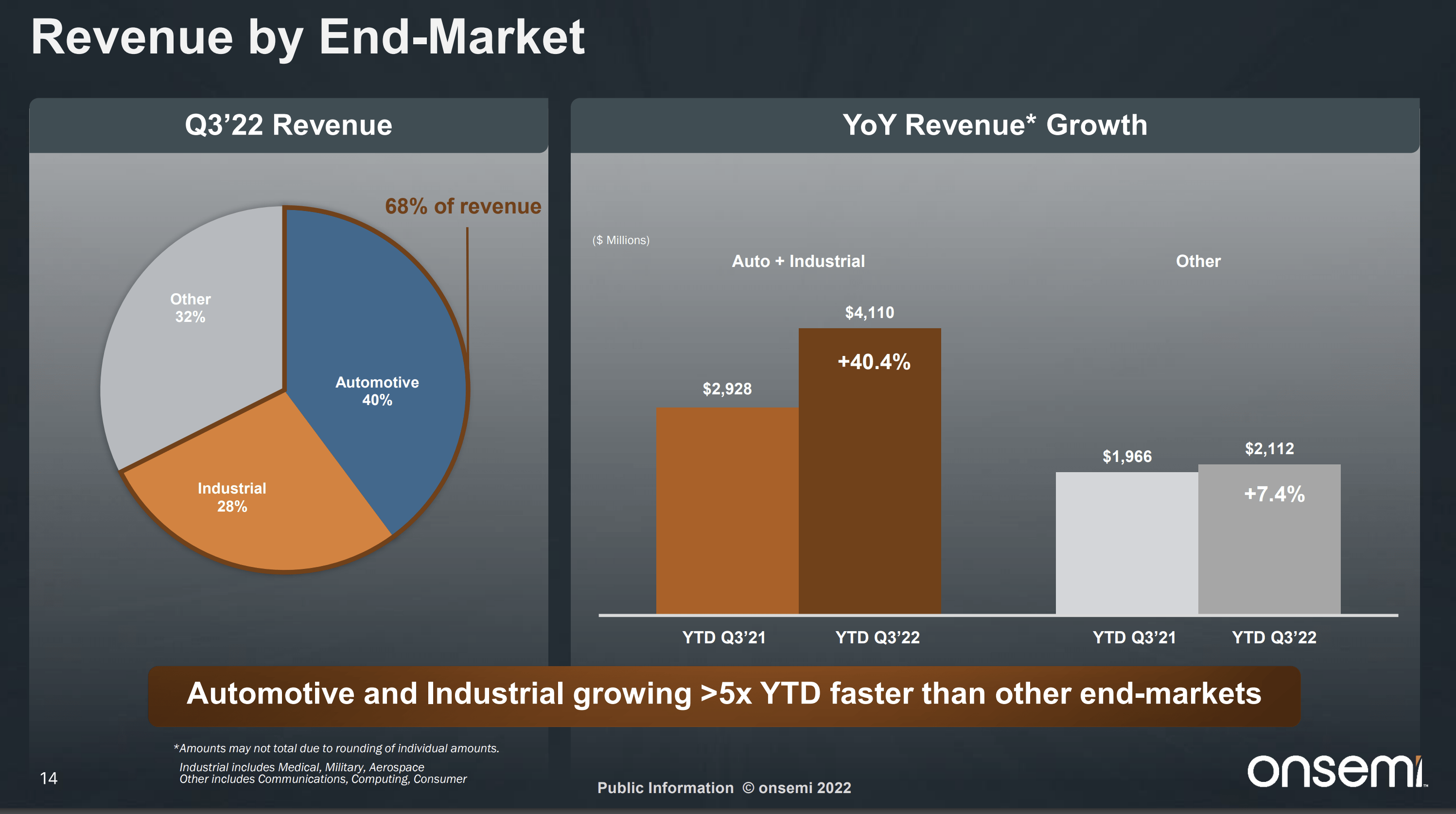

ON Semi grew revenue 26% year-over-year. Taking a closer look we can see that their automotive + industrial segments grew a whopping 40.4% year over year. This massive growth proves why they have chosen to focus their energy on those segments and they will likely be able to post strong growth numbers in those segments for the next few years.

ON Semi Q3 Earnings Presentation

{kind=link}

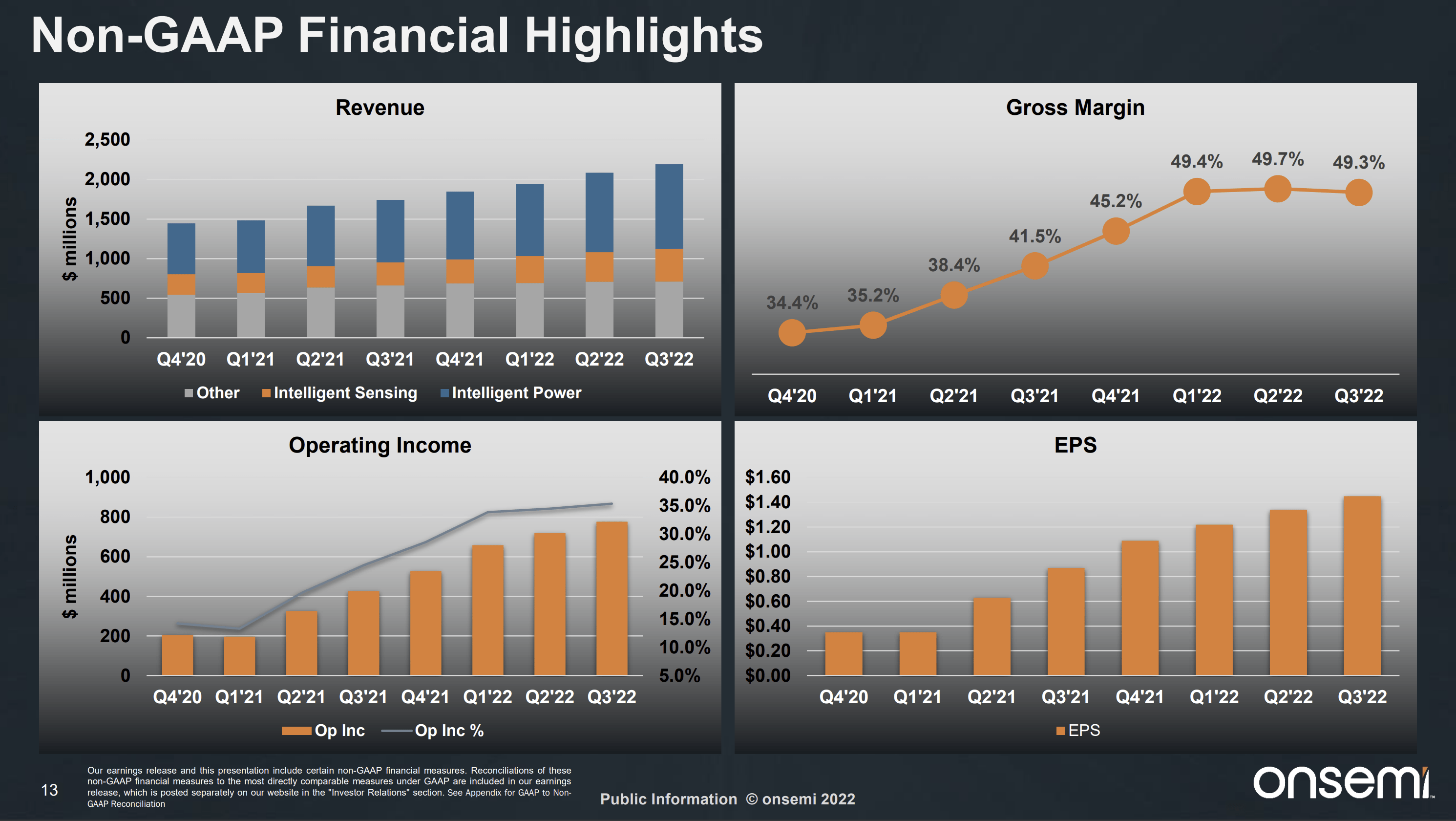

The margin compression that the analyst was concerned about is beginning to materialize. Their margins expanded rapidly before plateauing in recent quarters. Their gross margin is something to keep an eye on in the coming quarters and is expected to decrease slightly.

ON Semi Q3 Earnings Presentation

{kind=link}

Price Action

ON Semi has done very well over the past year. Not only are they outperforming the S&P 500, they are also outperforming many other semiconductor stocks. In a sector that has seen a massive drawdown in many stocks it’s nice to see a company that has held up so well.

Valuation

ON Semi is trading at a forward PE of 14.23. On a TTM basis the PE is 16.65, which is close to the levels it traded at in 2018 and 2019. Their business is in a significantly better place now than it was in the past and we believe it should be valued as such. We believe that ON should trade at a multiple of 20 times forward earnings to factor in their improved growth profile and reduced risk. This implies a price of $90.40 which would be an increase of 40.78% from these levels.

Risks

Some risks to this bullish take on ON Semi are:

ON might get outcompeted in the SiC market.

The trough of this semiconductor cycle may be deeper than the last one.

The economy could go into prolonged contraction.

ON may not be able to improve their manufacturing yields.

Geopolitical tensions could reduce demand and could hamper ON Semi’s ability to access manufacturing inputs.

Supply chain disruptions in China could ripple through the global economy.

If one or more of these risks materialize it would damage the bull case for ON Semi. As with all investment related risk an investors needs to assess their own time horizon and risk tolerance to decide for themselves if that investment is suitable. We believe the risk/reward is favorable at this time, but the risks must be respected. This is especially true in the semiconductor industry.

Key Takeaway

Long-term investors should not be deterred by the analyst downgrade even though they made some valid points. ON Semi is well positioned for success over the next decade and with good execution will become a leader in SiC. We believe now is a good time to buy shares provided the investor has a long time horizon.