The S&P 500 (SP500) on Friday retreated 0.66% for the holiday-shortened week to settle at 3,972.61 points, while its accompanying SPDR S&P 500 Trust ETF (NYSEARCA:SPY) also shed 0.66%.

The benchmark index’s weekly decline is the first of the new year, after having climbed more than 4% over the beginning two weeks of January.

Sentiment was weighed down by the release of economic data that showed signs of cooling in the U.S. economy and sparked off concerns over a growth slowdown. Though inflation data showed a moderation, the effects of the Federal Reserve’s monetary policy tightening are only showing up now and have led to worries that the central bank has been too aggressive and could tip the economy into recession.

The week’s economic calendar saw the release of the Empire State Manufacturing survey which showed a sharp contraction in business activity in January. Meanwhile, headline producer price inflation fell more than expected. Retail sales and industrial production slipped more than anticipated in December. The Philly Fed Business Outlook for January came in negative, while the number of Americans filing for weekly jobless claims surprisingly fell. Finally, there was data on the housing market in the form of building permits numbers and existing home sales figures.

Fed speakers through the week have indicated that the central bank will downshift its pace of rate hikes. According to the CME FedWatch tool, markets are now pricing in a 99.2% probability of a 25 basis-point hike at the monetary policy committee’s February meeting.

Market participants have also digested the start of the fourth quarter earnings season this week. Major names such as Goldman Sachs (GS), United Airlines (UAL), Alcoa (AA) and Procter & Gamble (PG) reported their results. Of note was Netflix (NFLX). The streaming giant’s financial performance was praised by analysts and the stock jumped on Friday, boosting broader equities.

Next week the earnings season will kick into a new gear. Companies of note scheduled to report include Tesla (TSLA), Microsoft (MSFT), Intel (INTC), Visa (V), Mastercard (MA) and Chevron (CVX).

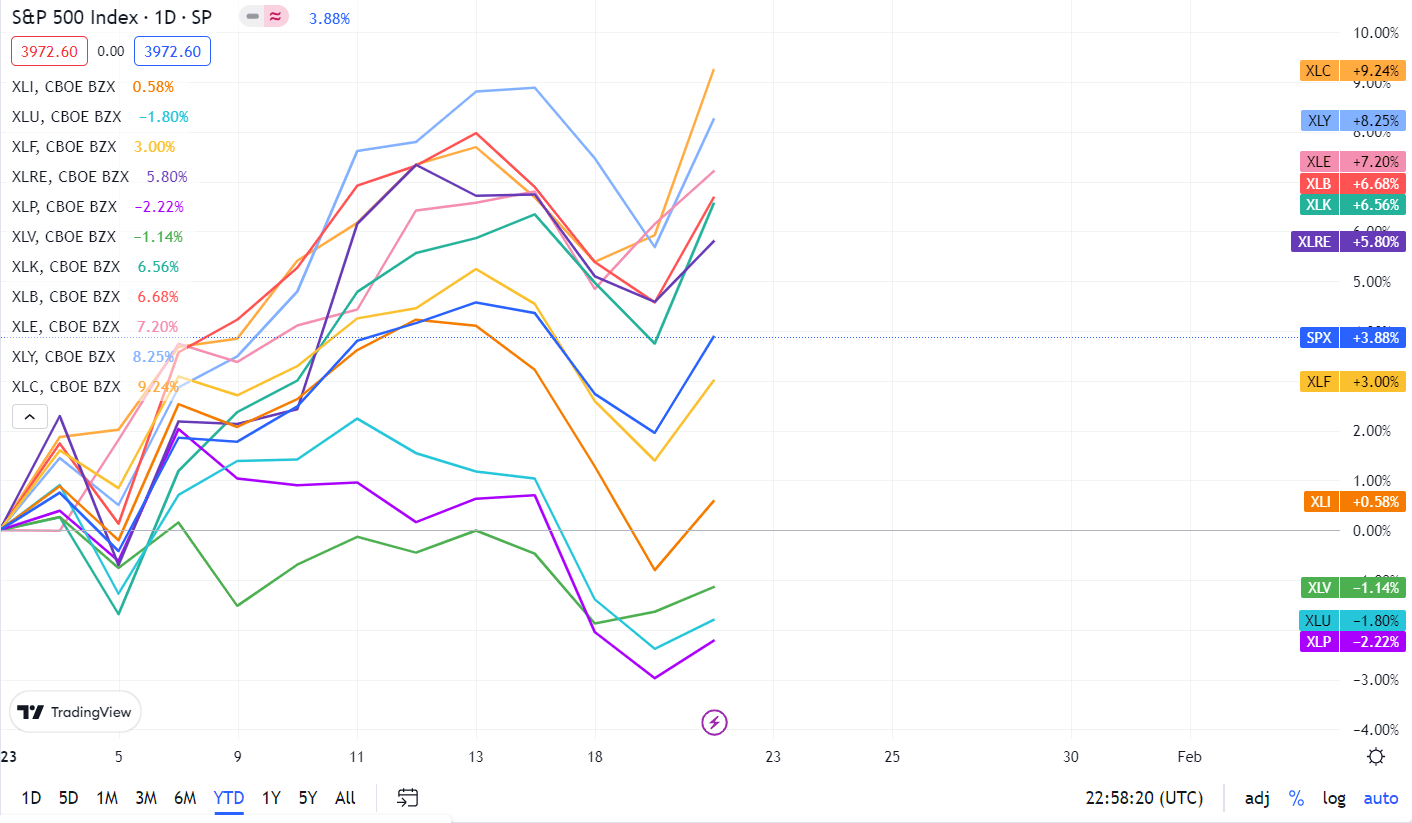

Of the 11 S&P 500 (SP500) sectors, eight ended this week in the red, led by Industrials and Utilities. Among the three gainers, heavyweight sector Communication Services added nearly 3%. See below a breakdown of the weekly performance of the sectors as well as their accompanying SPDR Select Sector ETFs from Jan. 13 close to Jan. 20 close:

#1: Communication Services +2.97%, and the Communication Services Select Sector SPDR Fund (XLC) +1.43%.

#2: Energy +0.74%, and the Energy Select Sector SPDR ETF (XLE) +0.59%.

#3: Information Technology +0.68%, and the Technology Select Sector SPDR ETF (XLK) +0.65%.

#4: Consumer Discretionary -0.51%, and the Consumer Discretionary Select Sector SPDR ETF (XLY) -0.52%.

#5: Real Estate -0.75%, and the Real Estate Select Sector SPDR ETF (XLRE) -0.86%.

#6: Health Care -1.12%, and the Health Care Select Sector SPDR ETF (XLV) -1.14%.

#7: Materials -1.21%, and the Materials Select Sector SPDR ETF (XLB) -1.21%.

#8: Financials -2.08%, and the Financial Select Sector SPDR ETF (XLF) -2.16%.

#9: Consumer Staples -2.86%, and the Consumer Staples Select Sector SPDR ETF (XLP) -2.84%.

#10: Utilities -2.93%, and the Utilities Select Sector SPDR ETF (XLU) -2.94%.

#11: Industrials -3.36%, and the Industrial Select Sector SPDR ETF (XLI) -3.39%.

Below is a chart of the 11 sectors’ YTD performance and how they fared against the S&P 500. For investors looking into the future of what’s happening, take a look at the Seeking Alpha Catalyst Watch to see next week’s breakdown of actionable events that stand out.

{kind=link}