AleksandarNakic/iStock via Getty Images

Co-authored with Long Player

As I plan for my retirement, I’m looking for ways to reduce my future workload so I can spend more time doing things I enjoy. This is why it is essential to own some “cash cow” and solid growth stocks; they require very little follow-up and can be held with confidence for decades.

So, I knew that as a retiree, the lowest maintenance companies pay a high yield, are investment grade, and have good growth potential. Such investments require less supervision, allowing me to spend my time figuring out how to spend all those dividends.

Today we’ll take a closer look at two Blue Chip companies currently paying a high yield, with strong balance sheets and great dividend growth potential.

Pick #1: Diamondback Energy – Yield 7.2%

Diamondback Energy, Inc (NASDAQ:FANG) is an independent oil and natural gas company headquartered in Midland, Texas, focused on the acquisition, development, and exploration of onshore oil and natural gas reserves in the Permian Basin in West Texas. FANG carries an investment-grade rating because of its prudent and disciplined management. This is a variable distribution entity with very fast growth. Source

FANG May 2023 Investor Presentation

{kind=link}

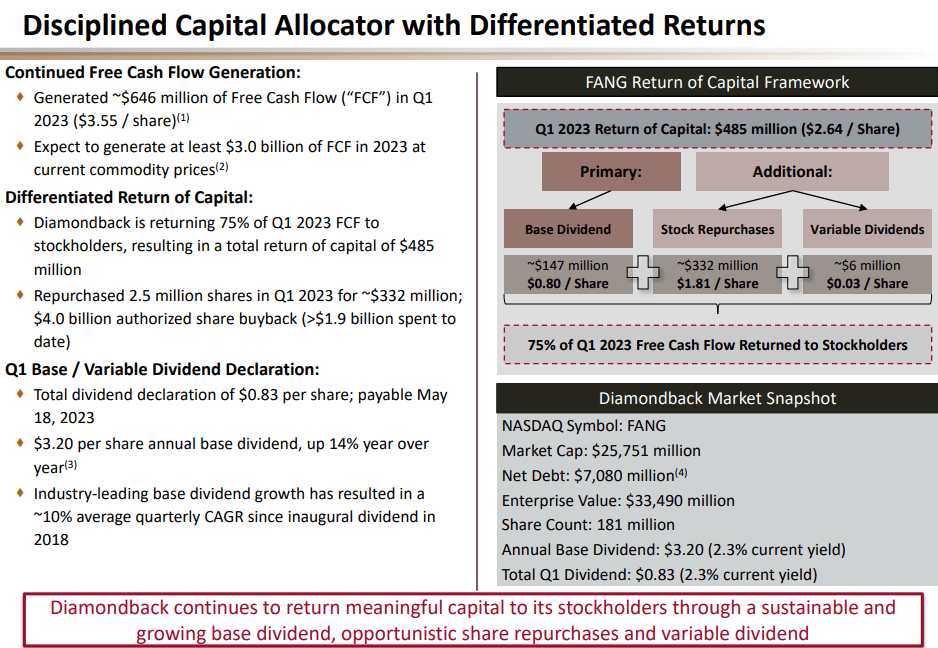

Diamondback has a fixed base dividend plus a variable component that will vary with the price of oil, or on their share repurchase program. The base dividend is currently $0.80 per share, ~2.5% yield at the current price. However, the base dividend has risen significantly over the past year (up 14% year-over-year) despite unfavorable oil price fluctuations. The variable component has averaged $1.50 in the last four quarters, ~4.7% yield for a combined 7.2% TTM yield.

Management also repurchases shares which is very accretive to shareholders. The key here is that management has a long history of acquisitions to keep rewarding shareholders with high dividends, and with share repurchases.

When FANG reported Q1 earnings last week, we learned that they took advantage of a more than $10 per share drop in price during the recent banking crisis as an opportunity to buy back more than 2 million shares rather than pay a variable dividend in Q2. That left about $.03 for the variable dividend this quarter. CEO Travis Stice summed it up this way:

Return of Capital: We generated $646 million of Free Cash Flow in the first quarter. With our commitment to return at least 75% of our Free Cash Flow to stockholders on a quarterly basis, this means we are going to return $485 million of Free Cash Flow for the quarter. Of this, $147 million is attributable to our quarterly base dividend of $0.80/share. Secondly, we repurchased $332 million worth of stock in the first quarter, which encompasses the majority of our post-dividend Free Cash Flow. This leaves $6 million, or $0.03 per share, for our variable dividend for the quarter.

The first quarter is exactly the reason we elected to implement a return of capital program with flexibility to allocate capital between share repurchases and a variable dividend. During the banking crisis and Silicon Valley Bank collapse, we took advantage of volatility and repurchased a significant amount of stock. In total, we repurchased 2.53 million shares for $332 million ($131.34 / share average) in the first quarter. – Shareholder Letter, May 1, 2023

Management plays the market-demand game of not growing production while returning a large share of cash flow to shareholders. But the acquisitions fill that growth need. Mr. Market loves a long-term growth story. So the current demand for return of capital is likely to fade as the realization that the 2015-2020 period is unlikely to repeat. But this company has a structure set up to continue the current program while meeting long-term demands for market growth that are likely to prevail in the future.

The acreage is above average in profitability. Therefore excess cash is likely to be used to increase production in addition to the acquisitions as market demands change over time. Source

FANG May 2023 Investor Presentation

Management balances the stock used in these transactions with the debt to make sure that financial ratios remain conservative after the transaction. In the meantime, production growth shown above is roughly 15%. That is a darn good growth rate for a company of this size. Per share growth of production is not far behind at 11%.

This means that while distributions will vary with the price of oil, the overall trend of those distributions will be up for the foreseeable future.

Diamondback management often acquires companies or lease holdings in areas that become “hot” before the prices reflect that “hot”. This is a management that will look for $65K per acre quality while often paying much less. Sometimes that price is as low as $20K an acre or less. This is exactly what shareholders pay management to do. But many managements do not execute the strategy either well or at all.

One of the things about variable distribution entities is the ability to switch from payments to stock repurchases if a deal happens. The second quarter will likely return to more payments to shareholders as another banking crisis is not anticipated. Much of the industry still expects liquids prices to increase in the second half of the year. Natural gas production is declining finally in the Haynesville Basin which is the swing area for natural gas. Therefore many expect natural gas prices to slowly strengthen going forward as rigs continue to be released in the Haynesville area.

Variable distribution entities are best looked at when there is less distribution as was the case this time. Management is setting the stage for a lot more distributions in the future.

Therefore, investors could see the dividend roughly double in the next 5 to 7 years as long as management pursues the current strategy. A well-run company like Diamondback is also a likely acquisition candidate down the road as purchasers love to buy companies that are not a problem. Good management like this one is often quite a bargain for shoppers in the long run. If you buy FANG, you are buying into the ‘blue chip’ of management in the Energy sector, and with high yields!

Pick #2: Simon Property Group – Yield 6.8%

Simon Property Group, Inc (NYSE:SPG) is the largest mall operator in the country. SPG reported earnings on May 2nd and had a great quarter and is raising guidance and raising the dividend 8.8% year over year.

The sheer diversification and the premier locations constitute a competitive moat that will likely last for years to come. Few competitors come close to matching these characteristics.

SPG Q1 2023 Supplemental Presentation

The resulting business performance has led to the investment grade ratings shown above that are also seldom matched throughout the industry. Similar ratios shown above demonstrate a considerable amount of financial flexibility. Clearly, this company will be able to access the debt market as needed and obtain some of the better interest rates in the process.

There have been some worries about the REIT sector with rising interest rates. SPG is somewhat isolated from those considerations by its premier locations that will likely outperform any industry challenges.

Management is very conservative, as is shown below: Source

{kind=link}

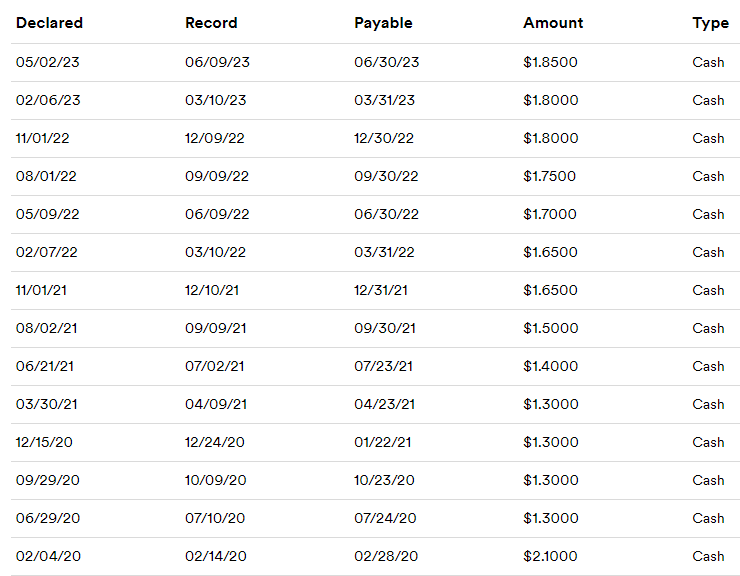

Management did cut the quarterly dividend in 2020, as shown above, when it became apparent that the economy would have to surmount some perceived headwinds. Years of increasing budget deficits combined with a lax Federal Reserve policy finally reared a very ugly prospect of inflation. Just as it takes years for inflation to appear, it also takes some time to whip the economy back into shape. Unfortunately, whipping the economy back into shape can be far more painful than the budget deficit-easy money “fun” was.

Despite all the concerns, the economy has been roaring along with record job creation. Inflation, meanwhile, has been slowly coming back in line despite concerns. Those who know that the CPI housing part of the calculation has a 1-year delay (very simplified) also know that housing which is nearly half of the CPI calculation has good news in store for inflation for the rest of this year (and then some).

As a result, the stock price correction appears to be overdone. This stock is nearly always a buy at under $120, and that is the case here. Management has been gradually restoring the dividend as the feared economic headwinds have not come to pass. There has been some inflation; however, that is slowly abating.

In the meantime, business is booming, and the finances are holding up better than the market expects. This is a “sleep well at night stock” as the business is never a concern. Management always keeps the finances conservative first and then distributes cash to shareholders.

The best part is that the dividend is likely to exceed the previous high once the inflation issues and worries about a recession pass. That is very likely to provide a generous return on the current price. REITs are best viewed as variable distribution entities. The time to consider them is when the distribution is low. Here, that distribution is still below the pre-cut level. Company finances indicate that the dividend can go far higher as economic headwinds continue to subside.

Summary

I have often found that the best results come from companies that trade based on a cheap valuation compared to their current cash flow and growth prospects. Both FANG and SPG are fantastic stocks. They operate good solid businesses, producing significant cash flow that is passed along to investors as dividends.

For a high-growth company, FANG has an unusually high yield of 7%. The U.S. is becoming an export hub for Europe and several other countries, and export demand from the U.S. will continue to grow. FANG has possibly the best management team in the Energy sector, with a focus on growth, dividends, and buybacks. The stock has a forward P/E of just six times, which is dirt cheap and offers significant upside potential.

As for our second pick, SPG has a 6.8% yield that is very well covered. Management will likely continue to raise that dividend back to previous levels of more than $2 per quarter (and probably further still). The financial strength rating gives this management a lot of leeway in planning growth to generate future dividends. This stock is trading at a discount to its usual valuation range. The price-earnings ratio alone is very cheap, and Simon rarely goes on sale.

At HDO we really like these two cheap high-quality stocks. We target similar ones for our ‘model portfolio’ which carries an overall yield of +9%. For retirees, the low price-earnings ratio strategy for solid stocks has been a time-honored way to outperform the market. There will likely be an additional valuation boost once interest rates begin their descent and return to their previous levels. That means these income plays have a capital appreciation component not often seen in the income sector. But that is very common when interest rates decline and is very good news for a retirement portfolio. These two picks need very little maintenance and are suitable for a retirement portfolio to buy and hold for the very long term!