Mongkol Onnuan

I started paying attention to the iShares Core Dividend Growth ETF (NYSEARCA:DGRO) in the summer of 2022. The idea of annual dividend growth is something many income investors strive for as it’s a fundamental aspect of their investment premise. When an individual company increases its dividend annually, it signals financial strength, and when investors are reinvesting the dividends, the annual increases will intensify the impacts of compound interest. DGRO takes the guesswork out of dividend growth investing and provides investors with an ETF that focuses on companies that have increased their dividends for a minimum of 5 consecutive years. DGRO has provided its investors with double-digit capital appreciation over the previous 5 years, downside mitigation throughout the bear market of 2022, and a dividend that has grown for 8 consecutive years. While there are many positives to DGRO, I feel there are fewer reasons to invest in DGRO today. We don’t live in a yield-starved environment, and income investors can almost double the 2.3% yield DGRO provides from a 2-year T-bill or a 1-year CD without taking on equity risk. For investors willing to take on exposure to equity risk, the Schwab U.S. Dividend Equity ETF (SCHD) has generated more capital appreciation than DGRO over the previous 5 years; its yield is a full percent larger, and grew the annual dividend for the past 10 consecutive years. Looking at DGRO independently, it’s an attractive ETF, but when making a decision about where to actually put capital, I don’t see a reason to invest in DGRO as it doesn’t standout in any particular area.

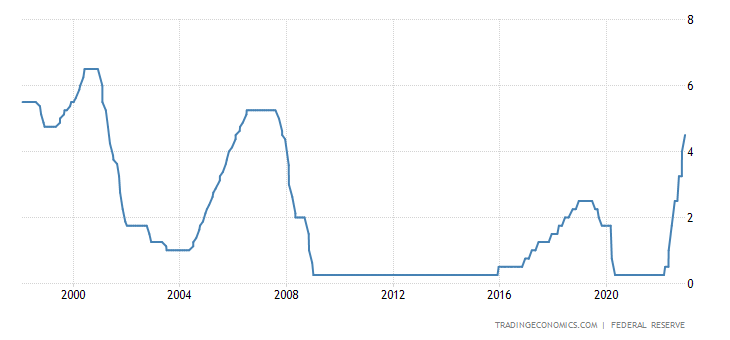

Income investors are living in a different world today where yield isn’t hard to find

There are many high-profile investments that don’t pay a dividend and have the allure for a significant return on investment over a long-term investment horizon, such as Amazon (AMZN), Tesla (TSLA), or Alphabet (GOOGL) (GOOG). Investors who focus on dividends are interested in generating income for the purposes of having an additional income stream, or using the dividends to reinvest and benefit from the powers of compounding interest.

Living in a low-yield environment throughout the majority of the previous decade and during the pandemic left fewer options for investors to generate yield. High-yield savings accounts, CDs, and T-bills weren’t attractive compared to investing in individual equities if generating income was a priority. Now that the Fed Funds Rate is approaching 5% with anticipated hikes on the way, it’s the largest interest rate seen in more than a decade. Investors that conduct adequate amounts of research prior to making an investment will see that investing in DGRO leaves money on the table, and this is the reason why I don’t see a reason to allocate capital toward DGRO.

{kind=link}

DGRO focuses on dividend growth, but if the fundamentals around dividend growth are inferior to SCHD, why not just invest in SCHD?

Here is the tale of the tape between DGRO and SCHD.

Annual Payout

- DGRO $1.17

- SCHD $2.56

Dividend Yield

- DGRO 2.3%

- SCHD 3.35%

Dividend Growth Rate TTM

- DGRO 2.3%

- SCHD 13.90%

Dividend Growth Rate 3Y (CAGR)

- DGRO 8.97%

- SCHD 14.10%

Dividend Growth Rate 5Y (CAGR)

- DGRO 10.61%

- SCHD 13.74%

Dividend Growth Rate 10Y (CAGR)

- DGRO –

- SCHD 12.20%

Consecutive Years of Dividend Increases

- DGRO 8 years

- SCHD 10 years

From a dividend growth rate perspective, there isn’t a single metric where DGRO outperforms SCHD. DGRO’s numbers are fantastic, and many investors would love these types of growth figures in their dividend payments, but SCHD overshadows them. Investors who allocate capital to DGRO rather than SCHD lose a full percentage point of yield right off the top. In the TTM, DGRO’s dividend growth trailed SCHD’s dividend by 11.6%; in the previous 3 years, the CAGR for DGRO’s dividend was 5.13% less than SCHD’s; and the CAGR over the past 5 years was 3.13% less than SCHD’s. If you’re investing in a fund based on dividend growth, why would you leave growth on the table? DGRO doesn’t deliver for its shareholders the way that SCHD does, and I don’t see a reason to leave 1.05% of dividend yield and several percentage points of CAGR on the table when SCHD is an option.

Outside of dividend growth, what would have happened to an investment of $10,000 in DGRO and SCHD over a 5-year period?

The only way I could make the exception and invest in DGRO rather than SCHD is if the overall investment superseded the growth aspects of the dividend. To determine this, I would need to see how the same amount of capital invested in DGRO and SCHD performed over the past 5 years and analyze the results. If DGRO captured enough additional appreciation, then there would be a reasonable rationalization to invest in DGRO as a dividend growth ETF over SCHD.

If you invested $10,000 in DGRO on 1/24/18, you would have purchased 272.55 shares. DGRO would have generated $5.01 per share in dividends, and by reinvesting them, your share count would have increased to 307.08. Your total annual dividend income would have increased by $138.44 or 62.68% as it went from $220.85 to $359.28. The investment today would be worth $15,606.28 for a return of 56.03%.

If you had invested the same $10,000 in SCHD on 1/24/18, you would have purchased 186.64 shares. This is where the extra yield and percentage points on the CAGR dividend growth come into play. SCHD generated $10.01 in dividends over the past 5 years, and by reinvesting the dividends, the total share count would have increased to 219.8. Your annual dividend income would have increased by $294.06 or 109.47% as it grew from $268.63 to $562.69. Today the $10,000 investment would be worth $16,820.24 for a total return of 68.23%.

{kind=link}

There wasn’t a single aspect of the investment where DGRO outperformed SCHD. Its total return trailed by -12.2%, and the projected annual dividend income growth trailed by -46.79%. If the statistics were reversed, then it would make sense to invest in DGRO rather than SCHD, but that’s not the case. SCHD has superior dividend growth aspects, and generated an additional 12.2% return on investment in 5 years.

Comparing the characteristics of DGRO and SCHD

DGRO tracks the US Dividend Growth Index from Morningstar, which is a dividend dollar-weighted index that seeks to measure the performance of US companies selected based on a consistent history of growing dividends. For a company to be eligible for the US Dividend Growth Index from Morningstar, the individual company must pay a qualified dividend, have a minimum of 5 consecutive years of annual dividend growth, and their earnings payout ratio must be less than 75%. DGRO’s investment parameters include investing at least 80% of its assets in the component securities of its Underlying Index and in investments that have economic characteristics that are substantially identical to the component securities of its Underlying Index. With the additional 20%, DGRO has the ability to allocate capital toward futures, options, and swap contracts, cash, and cash equivalents, including shares of money market funds.

SCHD tracks the Dow Jones U.S. Dividend 100 index. SCHD follows an investment premise that individual equities can’t exceed 4%, and a specific sector can’t exceed 25% of its assets. SCHD’s positions must have a minimum of ten consecutive years of dividend payments and a minimum float-adjusted market capitalization of $500 million. The Dow Jones U.S Dividend Index is evaluated by the highest dividend-yielding stocks based on cash flow to total debt, return on equity, dividend yield, and 5-year dividend growth rate. SCHD invests at least 90% of its assets in these equities and utilizes cash-flow to debt ratio, ROE, dividend yield, and dividend growth rate to make its decisions. SCHD is rebalanced quarterly to make sure its positions meet the 4% and 25% criteria, and the overall composition is reviewed on an annual basis.

DGRO has $24.92 billion in assets under management and charges an expense ratio of 0.08%. SCHD has $46.29 billion in assets under management and has an expense ratio of 0.06%. Over the past year, SCHD has declined by -1.92%, while DRGRO has declined by -4.07%. DGRO has less assets under management, charges a larger expense ratio, and has declined more than SCHD in the previous year.

Conclusion

I am not a shareholder of DGRO, and there is no reason for me to invest in DGRO for dividend growth when SCHD is outperforming DGRO in every aspect I have looked at. I am surprised that DGRO has $24.92 billion in assets under management, considering SCHD has the same overall goal. Investors are leaving capital on the table, investing in DGRO. Compared to other funds, or from a standalone point of view, DGRO has been a good investment and has achieved its goals. When comparing it to SCHD, it’s an inferior ETF, and my capital is better off in SCHD. I will be taking DGRO off of my watch list.