Helin Loik-Tomson/iStock via Getty Images

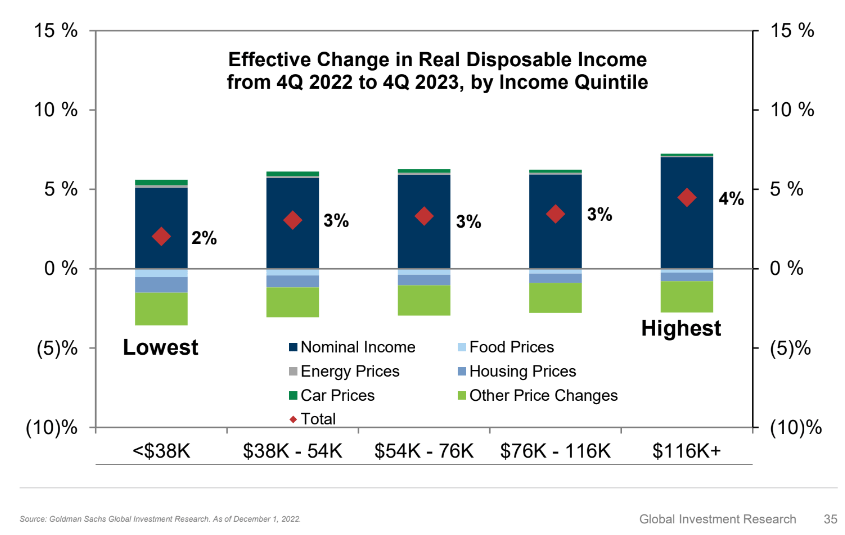

Better days are ahead for consumers. While there could be some pain in the employment market over the coming months, the unemployment rate currently rests at its lowest level since 1969 as real income growth has been negative for the last 21 months. That could change if forecasters at Goldman Sachs are correct. The research arm of the investment bank sees positive real disposable income across all five income cohorts in 2023. That could be a boon to higher-end retailers after 2022’s trade-down trend.

One firm caters to the higher price-point niche, but are shares of Sprouts worthy to be put in your shopping cart today? Let’s survey the aisles on this supermarket stock.

Rising Real Wages Expected In 2023

Goldman Sachs Investment Research

{kind=link}

According to Bank of America Global Research, Sprouts Farmers Markets (NASDAQ:SFM) is a natural & organic grocer with a small store (approximately 29,000 sq. ft.) format. After opening its first store in 2002, Sprouts has established itself as the 2nd largest natural & organic grocer, with 2021 sales of $6.1bn. With value-oriented stores that appear to be able to work across a wide variety of regions and income demographics, SFM could expand its store base from nearly 400 today to 1,200 longer term.

The Arizona-based $3.3 billion market cap Food & Staples Retailing industry company within the Consumer Staples sector trades at a low 13.7 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

Back in November, SFM beat on both earnings and sales estimates despite concerningly high and volatile food prices and exposure to the high-end consumer. Its EBIT margin came in at 5.7% vs the street forecast of just 5.0%. Even with competition from discounters like Walmart and Aldi, shares have managed to rise about 50% from their May low, capped off by a post-earnings surge. Recently, though, Wells Fargo mentioned the company as a ‘bottom five’ retailer at risk in their coverage.

On valuation, analysts at BofA see earnings having risen above the rate of inflation last year, but then settling back to under 7% in 2023. Per-share profits are then expected to bounce 10% in 2024. The Bloomberg consensus forecast is not as sanguine, though. Meanwhile, this high-growth grocer is not expected to pay dividends over the coming quarters.

Still, both Sprouts’ operating and GAAP earnings multiples are expected to be in the low to mid-teens through the next two years with decent free cash flow. Overall, I like the valuation here considering the growth prospects – the forward operating PEG ratio is just barely above one when if we normalized EPS growth to around 10%.

If we apply a multiple that is closer to the industry average, say, 15 on $2.50 of this year’s profits, then we get a valuation near $37.50, but there are risks, a continued inflationary environment could hurt the business. I’ll be keeping my eye on same-store sales numbers and how broader grocery inflation trends evolve this year. With improved margins reported lately, there are signs the management team is able to weather the volatile food price situation at the moment.

Sprouts: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

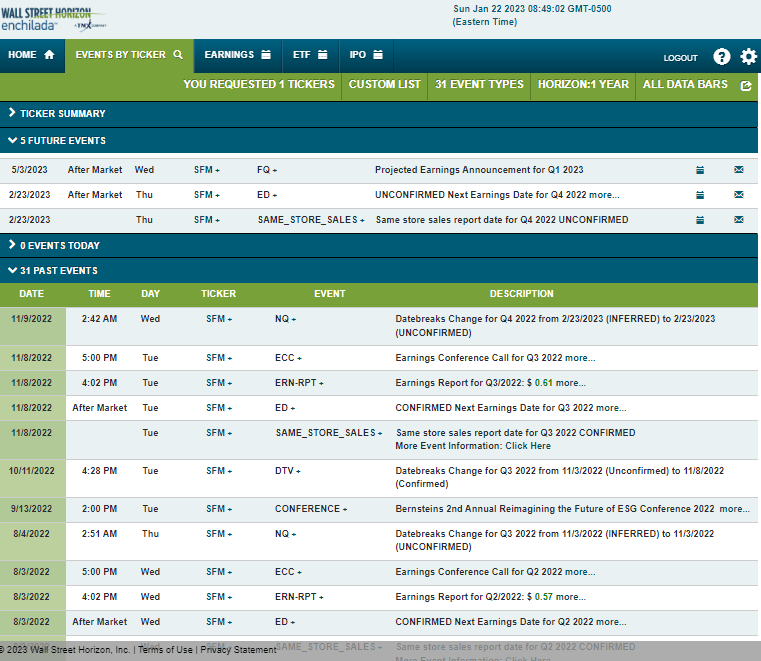

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, February 23 AMC. Same-store sales are also to be released in the quarterly report. The calendar is light on volatility catalysts aside from the earnings date.

Corporate Event Calendar

{kind=link}

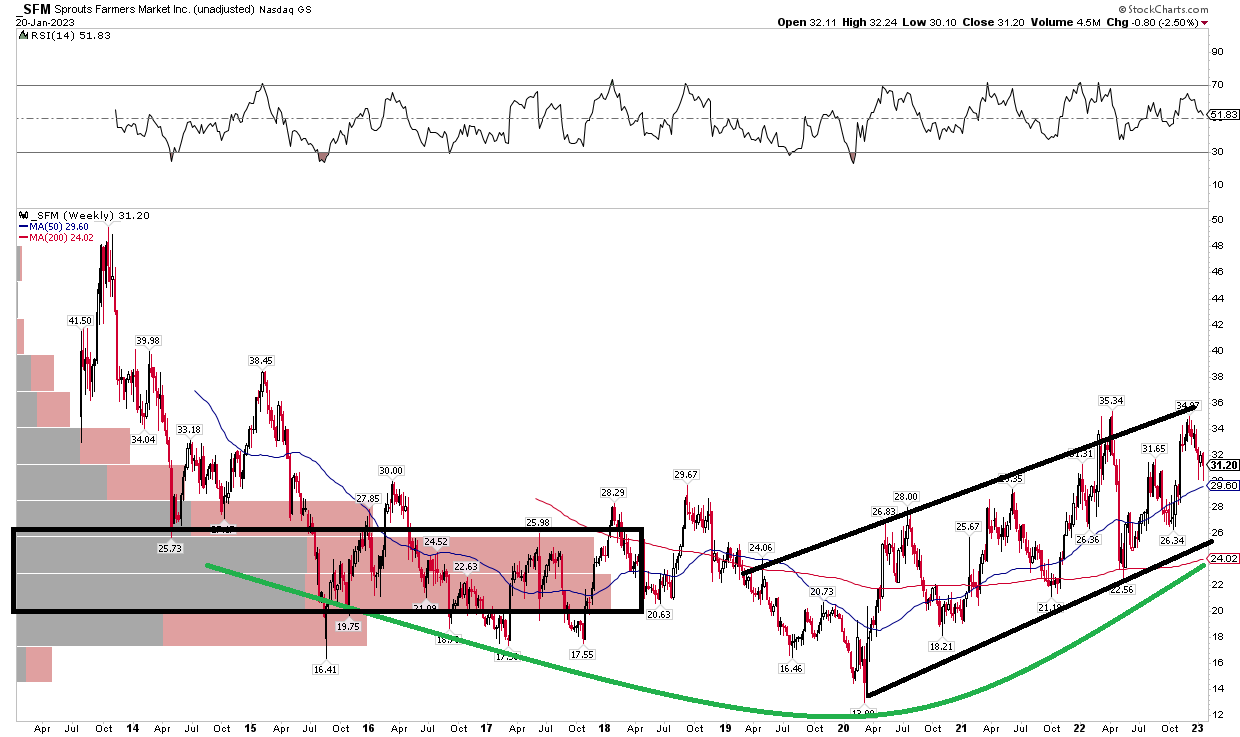

The Technical Take

I went long-term with the chart of SFM. Notice in the graph below that shares appear to be working on a bullish rounded bottom feature. The stock made a low back in March of 2020, like so many equities, and has risen steadily with eggs along the way. I see support and resistance via an uptrend channel – support is seen in the $24 to $26 area (above the long-term 200-week moving average) while resistance is in the $34 to $36 zone right now.

Also in the chart is significant volume-by-price in the $20 to $26 area which should offer support on pullbacks. Overall, the chart is constructive from a long-term perspective.

SFM: Bullish Rounded Bottom On The Weekly Chart

{kind=link}

The Bottom Line

With strong momentum and a decent valuation, I am bullish on Sprouts rising in the coming months and years. Robust margins help profitability despite an uncertain grocery environment with rising food prices.